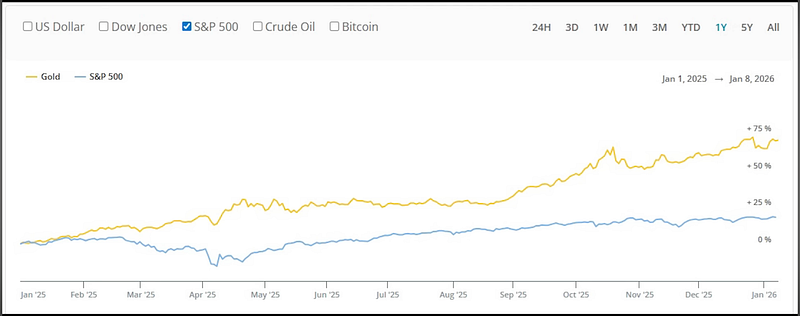

Gold has been on an absolute tear. Up roughly 64% in 2025, it has completely embarrassed the S&P 500’s 16% gain.

Everywhere you look, people are asking the same lazy question: “Is gold too expensive now?”

And every time I hear that, I feel like we’re missing the entire point.

Gold doesn’t crash because it gets “too expensive.” It crashes when confidence comes back to fiat money.

That distinction matters more today than it has at any point in the last decade.

What I want to do here is slow things down, zoom out, and actually think through why gold behaves the way it does, instead of reacting to price alone.

Because when you study history carefully, the current environment looks nothing like the conditions that produced gold’s biggest collapses.

The First Mental Model to be Clear on: Gold Is About Confidence, Not Price

The single most important thing to understand about gold is that it is not a growth asset. It is not a productivity asset.

It is monetary insurance.

Gold rises when people lose confidence in the purchasing power of money. Gold falls when that confidence is restored.

That’s it.

Everything else is noise.

Every major gold crash in modern history lines up perfectly with a moment when policymakers proved — credibly — that holding cash would once again pay you in real terms.

Not promises. Not forward guidance. Actual, painful policy decisions.

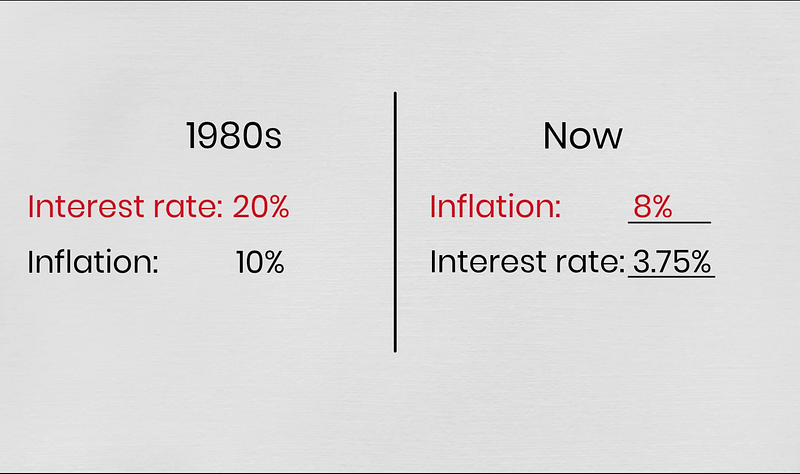

The 1980 Gold Crash

The classic example is 1980. Gold surged through the 1970s as inflation exploded, oil shocks rippled through the economy, and confidence in the U.S. dollar collapsed.

By January 1980, gold hit roughly $850 an ounce.

Then it crashed — hard — losing about 65%.

But here’s what people conveniently leave out.

Gold didn’t crash because it was “overvalued.” It crashed because the Federal Reserve, under Paul Volcker, did something almost unthinkable by today’s standards.

They raised interest rates to nearly 20%.

Not 5%.

Not 7%.

Twenty!!

For the first time in years, real interest rates turned meaningfully positive. Holding cash suddenly increased your purchasing power.

That decision caused a brutal recession. Unemployment soared. Businesses failed. The economy suffered.

But confidence in the dollar was restored. Gold didn’t stand a chance against that kind of monetary credibility.

The Post-2011 Decline: When the Fear Simply Didn’t Materialize

The second major gold collapse happened after 2011.

Gold peaked around $1,920 an ounce during the aftermath of the global financial crisis.

The narrative back then was simple: Quantitative easing would cause runaway inflation.

Fiat currencies would be debased. Gold would protect you.

Except… inflation never showed up.

Globalization kept wages down. Excess capacity suppressed pricing power. Technology acted as a deflationary force.

As it became clear that inflation wasn’t coming, the need for monetary insurance faded. The Federal Reserve slowly signaled an exit from emergency policy.

Real rates began to rise. The dollar strengthened.

Gold didn’t crash overnight this time. It bled slowly — down about 45% by 2015.

Once again, the driver wasn’t price. It was restored confidence.

Why Today Is Fundamentally Different

Now let’s talk about today. Because this is where old mental models completely break down.

Right now, real interest rates are still negative. Nominal rates might sit around 3.75–4%, but inflation across many sectors remains closer to 6–7%.

That means holding cash still erodes purchasing power.

In the past, gold crashes required sustained positive real yields. We don’t have that.

And here’s the bigger constraint no one wants to confront.

U.S. government debt.

In 1980, debt-to-GDP was roughly 30%. Today, it’s north of 120%.

The U.S. government is running fiscal deficits approaching $1.8 trillion in FY2025. Raising rates aggressively enough to replicate a Volcker-style reset would explode debt servicing costs.

Politically, economically, and structurally, that option barely exists.

Which brings us to the uncomfortable conclusion: Monetary credibility today is weaker, not stronger.

Central Banks Are Telling You the Same Story

One of the most underappreciated signals in the gold market right now is who is buying.

Central banks.

They are buying gold at record levels. Not trading it. Not hedging. Accumulating it.

This did not happen in 1980. It did not happen in 2011.

Central banks don’t buy gold because it’s fashionable. They buy it because they’re thinking in decades, not quarters.

And increasingly, they are thinking about diversification away from dollar dependence. That doesn’t mean the dollar is collapsing tomorrow. But it does mean its long-term dominance is no longer taken for granted.

Gold thrives in that uncertainty.

Real Interest Rates

If you strip everything down to one variable, it’s real interest rates.

When real rates are negative, gold tends to rise. When real rates turn sustainably positive, gold struggles.

Right now, real rates remain negative. And given the fiscal backdrop, keeping them positive for long would require economic pain few policymakers are willing to accept.

That doesn’t mean gold goes straight up forever. Markets never work that way.

It does mean that a structural crash requires conditions that simply are not present.

What Would Actually Need to Happen for Gold to Crash?

History is very clear here.

A major gold crash would require all of the following:

• Sustained positive real interest rates

• A strong, multi-year U.S. dollar bull cycle

• Restored confidence in monetary and fiscal discipline

• Central banks selling gold, not buying it

• Political willingness to accept recession and unemployment

None of those boxes are meaningfully checked today.

Some could change at the margin. But all of them aligning at once feels improbable.

So What Is Likely From Here?

This is where nuance matters.

A lack of crash conditions does not mean a straight-line rally.

The most realistic scenarios look like this: Gold could enter a period of sideways consolidation. After a 64% annual move, digestion is normal.

Gold could experience sharp corrections — 15% or more — within an ongoing bull market. That has happened many times historically without breaking the larger trend.

What looks unlikely is a repeat of 1980 or 2011. Those collapses required restored faith in fiat systems that, frankly, no longer inspire the same confidence.

There’s a reason the Weimar Republic keeps coming up in discussions like this. Fiat currencies backed by nothing ultimately rely on trust. When that trust erodes, the currency doesn’t fail in a straight line — it fails in waves.

Gold didn’t go up smoothly in Weimar Germany. It corrected. It consolidated. It shook people out.

But over time, it preserved purchasing power while the currency didn’t.

That doesn’t mean hyperinflation is around the corner. It does mean that gold’s role as monetary insurance hasn’t disappeared just because the price is higher.

Final Thoughts: Stop Thinking in Headlines, Start Thinking in Systems

Gold doesn’t care about your chart patterns. It doesn’t care about round numbers. It doesn’t care that it’s “up too much.”

It responds to systems — monetary systems, fiscal systems, and credibility.

Right now, real rates are negative. Debt levels are historically extreme. Central banks are accumulating gold, not distributing it. Fiscal discipline is more rhetoric than reality.

Could gold correct? Absolutely.

Could it crash the way it did in 1980 or after 2011? That would require a political and monetary regime shift that simply doesn’t align with today’s constraints.

The mistake I see over and over is people assuming price alone determines risk. History shows the opposite.

Gold falls when confidence returns. And right now, confidence in fiat money remains fragile — no matter how uncomfortable that truth might be.

That’s the lens I’m using. And until that lens changes, gold still makes sense — not as a trade, but as insurance in a system that keeps testing its own limits.