I’ve been watching this gold and silver rally with a mix of fascination and discomfort.

Not because it isn’t impressive. It absolutely is. Gold above $5,000 an ounce. Silver north of $100.

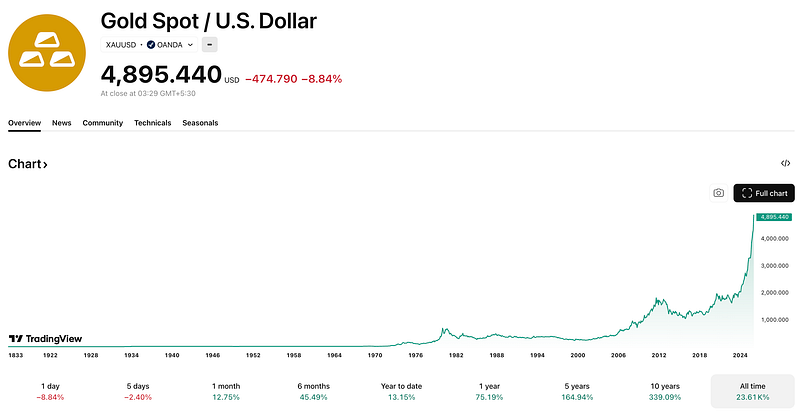

Those are numbers that, until recently, sounded almost absurd. These are not assets known for explosive moves. They’re supposed to be slow, boring, and defensive.

And yet here we are, watching precious metals behave like high-beta risk assets.

That alone should make anyone pause.

Because when traditionally “stable” assets start going vertical, it’s usually not a sign of safety. It’s a sign that something deeper is happening beneath the surface.

So I want to talk through what I think is really driving this move, why the popular explanations fall short, and — most importantly — why I’m personally not rushing to rotate capital into gold and silver here, even though the charts look unstoppable.

The Story Everyone Is Telling — And Why It’s Incomplete

The mainstream narrative is simple.

Geopolitics.

Debt.

Deficits.

The Fed.

Safe haven demand.

We’ve heard this story for years. And that’s exactly the problem.

None of these forces are new.

The U.S. has been running deficits for decades.

Geopolitical tensions didn’t suddenly appear this year.

Central banks have been experimenting with policy since 2008.

If those factors alone were enough to send gold to $5,000 and silver to $100, we would have seen this move long ago.

So when price action becomes this extreme, I stop asking what sounds logical and start asking what actually changed.

And what changed isn’t investor psychology first.

It’s supply.

The Real Driver: Government Stockpiling and a Supply Squeeze

This rally didn’t start with retail investors. It didn’t even start with hedge funds.

It started quietly, at the government level.

The United States officially designated silver as a critical mineral for national security late last year. That single classification changed everything.

Once silver was labeled essential for defense, energy infrastructure, AI, semiconductors, EVs, and solar, it triggered a wave of federal procurement. Large. Urgent. Non-price-sensitive.

At the same time, China imposed a complete export ban on silver.

Not a quota. Not a tariff. A full stop.

China isn’t doing this to speculate. They’re doing it to lock down supply for domestic technology and energy production.

Now combine those two forces:

The U.S. aggressively buying

China refusing to sell

And suddenly you have a global supply squeeze in one of the smallest major commodity markets on Earth.

Silver doesn’t have the liquidity depth of oil or gold. When large buyers step in, the market doesn’t adjust smoothly — It gaps.

That’s how you get vertical moves.

Gold is experiencing a similar, though slightly less violent, dynamic. Central banks — especially the U.S. and China — are treating gold like a strategic reserve asset again, closer to oil than a passive store of value.

This isn’t fear-driven buying. It’s policy-driven accumulation.

And once price starts moving, investors pile in, assuming the rally must be “macro-justified.”

That’s where the danger begins.

When Price Goes Up, but Risk Gets Worse

Here’s where I start to get uncomfortable.

Returns look incredible on the surface. But when you adjust those returns for risk, the picture flips completely.

The Sharpe ratio tells that story clearly.

Silver’s Sharpe ratio is now the highest it has ever been.

Higher than the 1980s.

Higher than the 2011 peak.

That doesn’t mean silver is “strong.” It means you are being compensated less and less for the volatility you’re taking on.

Historically, every time silver’s Sharpe ratio reached these levels, it marked the end of the trade, not the beginning.

Gold’s Sharpe ratio is also flashing warning signs. It’s sitting at levels last seen in 1980 and 2011 — both major long-term tops.

This isn’t subtle. It’s textbook late-cycle behavior.

The 200-Day EMA: When Distance Becomes Risk

Another metric I pay close attention to is how far price stretches from its long-term mean.

For both gold and silver, that mean is the 200-day exponential moving average.

Silver is currently trading at nearly four times its 200EMA. That has never happened before.

Gold is also at its most extended level relative to its 200EMA since 1980.

In markets, extreme distance from equilibrium doesn’t mean strength. It means fragility. At these levels, price doesn’t need bad news to fall. It just needs buying pressure to slow down.

The last time precious metals behaved like this was around 1980.

That period had everything:

Double-digit inflation

Stagflation

Oil crises

Geopolitical chaos

The collapse of Bretton Woods

It felt like the monetary system itself was breaking.

Gold and silver went parabolic.

And then they collapsed.

On an inflation-adjusted basis, those highs were never sustainably reclaimed.

That’s the uncomfortable truth most precious-metal bulls avoid discussing.

Gold and silver protect purchasing power over very long periods. They do not reliably compound it. They are preservation tools, not growth engines.

What I’m seeing now feels eerily similar to past euphoric moments in other markets.

People aren’t buying gold and silver because they’ve modeled long-term cash flows or real yields. They’re buying because price is going up and narratives feel comforting.

That’s the same psychology that drove:

Bitcoin in 2017

Meme coins in 2021

Tech stocks at every major peak

When assets meant to be conservative start attracting speculative momentum, something is off.

Logarithmic Risk Tells the Same Story

I like logarithmic risk because it scales across market caps and price levels.

It lets you compare apples to apples.

Right now:

Silver is at 100% logarithmic risk

Gold is around 94%

Bitcoin is roughly 30%

That’s not a typo. Bitcoin — despite being volatile, unloved, and out of favor — has dramatically lower risk by this measure than gold or silver at current levels.

In 2017, Bitcoin’s risk peaked near 97% — That was a top.

Today, it’s nowhere near that.

This Changes How I Think About Allocation

None of this means gold and silver are “bad.” They serve a purpose.

But deploying fresh capital into assets sitting at historic risk extremes rarely ends well.

The irony is obvious. The assets that feel safest emotionally are often the riskiest financially.

Bitcoin doesn’t feel comfortable right now. It’s volatile. It’s unpopular. It’s questioned.

That’s usually when risk-adjusted opportunities start forming — not when CNBC is celebrating new highs in assets that haven’t moved in decades.

So What Am I Doing Instead?

I’m not chasing gold. I’m not chasing silver.

I’m respecting the move — but not participating in it at these levels.

From a risk-adjusted perspective, Bitcoin offers asymmetry that precious metals simply don’t right now. Even with downside risk, the reward potential relative to risk is meaningfully better.

Based on this framework, a medium-term target for Bitcoin is near $120,000 — not because of hype, but because of probabilistic risk modeling.

That doesn’t mean it happens tomorrow. It means the math favors patience over panic.

This rally in gold and silver is real. It’s historic. And it’s driven by forces most investors never see.

But history is clear: When risk metrics scream “extreme” and price action seduces capital at the same time, the smart move is restraint, not excitement.

I’d rather be early and uncomfortable in an asset with expanding upside than late and euphoric in one where risk has already been pulled forward.

Sometimes the hardest trade is the one you don’t take.