Photo by Kanchanara on Unsplash

Over the past few weeks, I’ve found myself questioning things I used to take for granted about markets.

Not just crypto, but gold, stocks, tech, and even how I think about capital allocation and lifestyle choices. And the more I dig into the data, the more convinced I am that it is different — not in the “this time is different” meme way, but in how participants are behaving and how risk is being priced.

Bitcoin, altcoins, gold, and equities are all telling pieces of the same story.

And that story is not one of easy upside.

Starting with BTC: The Price Isn’t the Question — The Structure Is

Let’s start with Bitcoin, because everything still flows from it.

Bitcoin crashed hard on February 6, dropping to around $60,000. It bounced toward $70,000 shortly after, and then rolled over again.

The obvious question everyone keeps asking is simple:

Was that the bottom?

But I think that’s the wrong question. The better question is whether Bitcoin has done what it historically does in bear markets.

And the honest answer is: not yet.

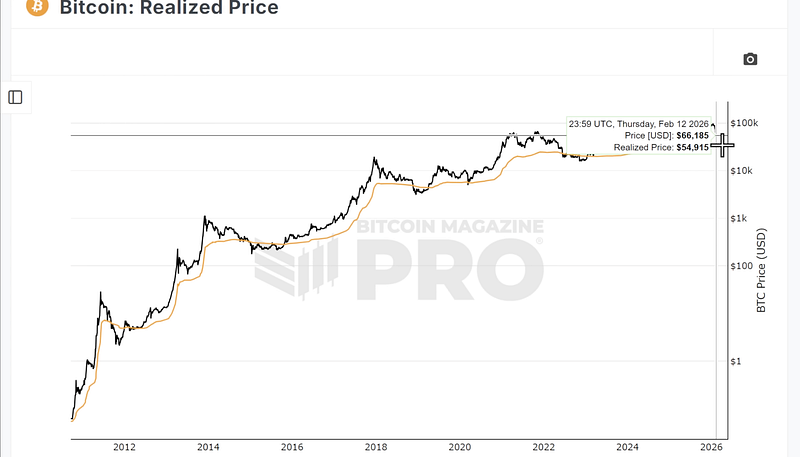

What the Bottom Models Are Actually Saying

There are a few Bitcoin price models I still respect because they’re rooted in on-chain reality, not vibes.

The realized price is still intact. Historically, that’s a meaningful support. But Bitcoin isn’t anywhere near it yet.

The balance price, which reflects mining economics, points toward roughly $40,000. That doesn’t mean price must go there, but historically, bear markets have tested that region or worse.

Then there’s the CVDD bottom indicator, which steadily rises over time and currently suggests a bottom closer to $47,000.

When I layer all of this together, I don’t see confirmation that the bear market is finished. What I see is a market that’s only about halfway through a typical drawdown.

Historically, Bitcoin bear markets have erased 70–90% from peak to trough. This one has only corrected around 50% so far.

That matters.

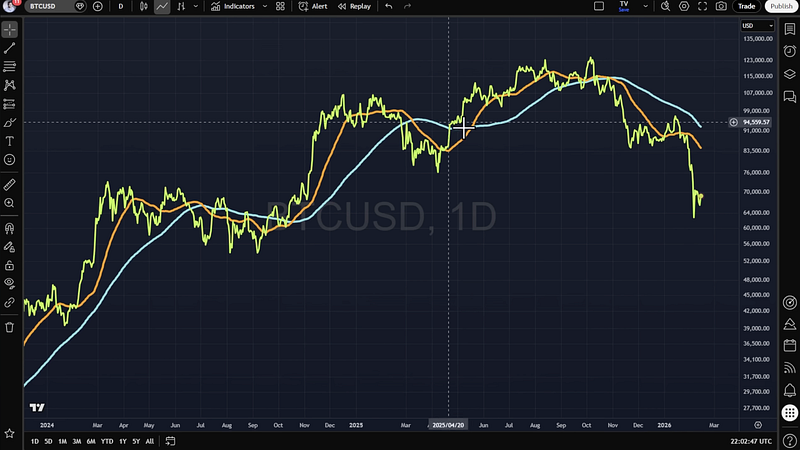

Momentum Confirms the Same Thing

I also pay attention to simple trend tools, not because they’re perfect, but because they keep me from fighting the tape.

Bitcoin remains below both the 44-day and 125-day simple moving averages. That’s a bearish signal. Not catastrophic, but clear.

When price is below trend and valuation models are still above historical bottoms, I don’t feel the urge to “be brave.” I feel the urge to wait.

How I’m Actually Positioning Around Bitcoin

I don’t treat all time horizons the same.

If you’re trading days or weeks, sure — dips can be traded. Volatility cuts both ways.

But if your horizon is months or longer, this is not where I want to deploy size.

My rule has stayed consistent across cycles:

In bear markets, I short tops.

In bull markets, I buy dips.

I do not buy aggressively against the macro trend.

Right now, the macro trend is still down.

That’s why I’m far more interested in Bitcoin in the $40K–$50K zone than anywhere near current prices.

That range offers asymmetry. Current prices don’t.

Altcoins — I’m Not Touching Them

I’m holding zero altcoins right now.

That’s not because I hate them. It’s because altcoins are simply leveraged Bitcoin in disguise.

If Bitcoin drops another 20–30%, most altcoins will drop much more. They always do.

Until Bitcoin:

Reclaims key moving averages, and

Establishes a clear uptrend;

Altcoins are just a faster way to lose capital.

I’d rather miss the first leg than catch a falling knife.

Gold — A Hedge, Not a Bet

Gold is one of those assets people talk about emotionally. I try not to.

Historically, gold has been a decent diversifier, not a compounding engine. It shines when other assets collapse.

But valuation matters.

Gold vs Money Supply Tells an Uncomfortable Story

When I look at gold relative to the U.S. monetary base going back to 1959, gold doesn’t look cheap anymore.

In fact, it looks expensive.

Gold supply grows roughly 2% per year through mining. The money supply has grown closer to 6.8% annually.

Over very long periods, that implies gold should appreciate around 5% per year in fiat terms.

And historically, that’s exactly what happened — including long periods of underperformance.

At current levels, gold could theoretically fall 40–50% just to revert to its long-term equilibrium versus money supply.

That doesn’t mean it will. But it does mean I’m not buying gold here expecting upside.

For me, gold belongs in a 2–5% hedge allocation, not as a growth asset.

The same caution applies to silver.

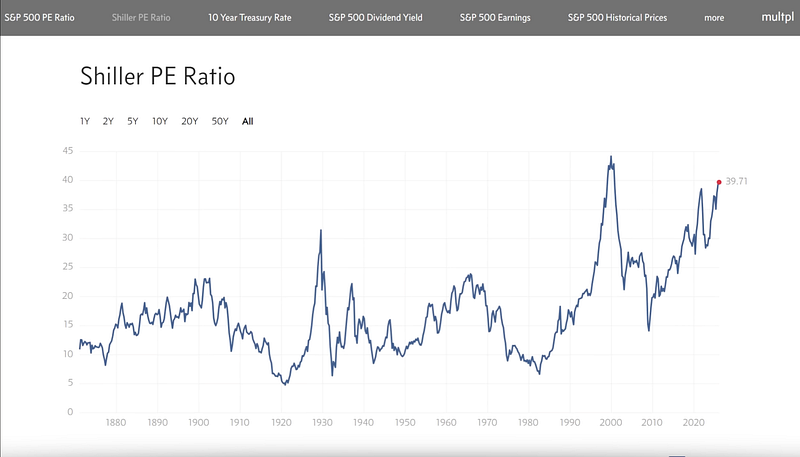

Stocks and Tech: Expensive Without the Euphoria

The stock market, especially tech, is another area where narratives are getting ahead of reality.

Valuations, measured by price-to-earnings ratios, are near levels last seen around the dot-com peak.

And yet, something important is missing — Momentum.

This Isn’t 1999

Despite all the AI hype, we don’t see the kind of vertical, speculative mania that defined the late 1990s.

Major tech names like Microsoft, Amazon, and Meta haven’t meaningfully outperformed the NASDAQ over the long term.

In fact, many of them could still fall 40–60% relative to the indexwithout breaking historical norms.

That’s why I prefer broad exposure through ETFs like QQQ rather than betting heavily on individual names.

Diversification matters more when valuations are stretched.

Tokenization: Powerful Idea, Messy Reality

Tokenization of real-world assets gets sold as inevitable. I’m more skeptical.

The idea is simple: tokenize treasuries, real estate, credit, and even stocks. The problem is everything around it. Tokenization bypasses capital controls. It muddies AML enforcement. It creates massive incentives for insider trading and information asymmetry.

Private credit tokenization worries me the most. Issuers get paid to issue more debt. Buyers often don’t understand the risk they’re taking.

That’s not innovation — that’s misaligned incentives on-chain.

Regulation will push back, especially around tokenized equities.

Tokenization will happen, but slowly, selectively, and with far more friction than people expect.

How I’m Managing My Portfolio Right Now

I’m playing defense.

It means patience.

I’m heavily allocated to cash and fixed income, earning yields that partially offset inflation. I keep spot Bitcoin separate from trading strategies. Spot is long-term. Derivatives are tactical.

I’m open to shorting overvalued assets, including equities, rather than buying dips in a bearish macro environment.

I avoid complex yield pools and altcoin exposure.

And I maintain diversification across assets that don’t all move together.

That flexibility lets me buy when things actually get cheap.

Bitcoin Targets: Downside First, Then Upside

My base case hasn’t changed.

I expect Bitcoin to find a durable bottom somewhere between $40K and $50K.

If and when that happens, the upside becomes compelling.

Over a full cycle, Bitcoin reaching $200K–$300K is plausible. But I wouldn’t ride it blindly.

Historically, profit-taking makes sense around $200K–$250K, well before euphoric blow-off tops.

Risk-to-reward matters more than predictions.

The Missing Ingredient: Capital Inflows

One last thing keeps me cautious. Stablecoin market cap hasn’t expanded since October 2023. That means no fresh retail capital.

Without new money, rallies fade. Sustained bull markets don’t happen. Bitcoin and stocks remain correlated. If equities suffer a systemic drawdown, Bitcoin will likely overshoot to the downside.

That’s just reality.

Final Thoughts

I don’t think we’ve seen the bottom yet.

Bitcoin hasn’t reached historical valuation zones. Momentum is still bearish. Altcoins remain vulnerable.

Gold, Silver, and tech are expensive.

Tokenization is overhyped in the short term.

That doesn’t make me bearish forever. It makes me patient. The best opportunities come when conviction collapses — not when fear first appears.

And I’m willing to wait for that moment.

Found this article insightful?

It would mean a lot if you could give it a clap and follow for more financial alpha, which “influencers” are too lazy to study and share.🌟

Follow me on Twitter/X to stay always up to date.🎄